Knowledge sharing

Sunday, December 27, 2015

Sunday, December 20, 2015

Friday, December 11, 2015

UK Tax administration: large businesses transparency strategy

HM Revenue and Customs (HMRC) is committed to dealing with all customers fairly and efficiently while making sure that the correct tax is paid to the Exchequer. HMRCʹs Large Business Directorate manages the largest 2,000 or so businesses using a risk based approach. This is due to their size and complexity, the tax at stake, and the consequent risk they present to the Exchequer.

This measure seeks to encourage tax transparency and compliance across all large businesses. To achieve this, we are introducing the requirement for qualifying large businesses to publish their tax strategy in relation to UK taxation.

This legislation will includes details of the tax strategies required to be published by such large business together with details of where and when publication is required and details of penalties for non‐compliance.

General description of the measure

The measure will introduce a legislative requirement for all large businesses to publish an annual tax strategy, in so far as it relates to UK activities, approved by the Business’s Executive Board.

The strategy will cover 4 areas:

- the approach of the UK group to risk management and governance arrangements in relation to UK taxation

- the attitude of the group towards tax planning (so far as affecting UK taxation)

- the level of risk in relation to UK taxation that the group is prepared to accept

- the approach of the group towards its dealings with HM Revenue and Customs (HMRC)

Non-publication of an identifiable tax strategy or incomplete content based on the 4 areas outlined above could lead to a financial penalty. This penalty will be subject to the usual HMRC appeals process.

Who is likely to be affected

Around 2,000 largest businesses in the UK.

Policy objective

The publication of tax strategies will ensure greater transparency around a business’s approach to tax to HMRC, shareholders and consumers. And board level oversight of those strategies will embed tax strategy in existing corporate governance processes. Taken together this should drive behaviour change around tax planning and therefore enhance tax compliance.

Proposed revisions

Legislation will be introduced in the Finance Bill 2016 to require qualifying large businesses or qualifying groups to publish a tax strategy, in relation to UK taxation, on the internet.

The legislation sets out the content required for inclusion in the tax strategy.

The strategy will need to remain accessible until the next update to the strategy, typically on an annual basis. A penalty may be chargeable either for the non-publication of a tax strategy or if the information contained within the published strategy does not meet the requirements of the legislation.

Monitoring and evaluation

This measure will form part of HMRCs business risk review processes and implementation and impact will be measured within the internal governance and risk management processes within Large Business Directorate.

Thursday, December 3, 2015

Interim VAT Management

Are you looking for a seasoned professional?

Do you need to manage a project about to start?

Are you facing a temporary shortage of resources?

Interim management is most helpful where a specific project is run where the interim manager can independently focus its time and is particularly helpful when resources are needed to meet specific deadlines.

As part of our interim management services, we make our highly qualified and experienced professionals available to you with a schedule tailored to your needs. We have extensive experience serving senior roles in a variety of industries and organizations.

We are best fit to develop and implement short term action plans and provide the opportunity to implement long term strategic and operational solutions.

Benefits of our interim management service

- We will bring you the best experts who create value from day one

- We have wide-ranging industry experience

- We will charge you by the hour for the time we spend working on your assignment

- Flexible working hours

- Our interim managers have completed several challenging assignments, bring with them a high technical and operational background, great work ethic and motivation

- They can look tax and accounting processes from the outside

- They work responsibly, diligently and efficiently

We not only develop but also implement solutions

VAT reporting

Business challenges

- Businesses may not have a VAT person and need someone to manage their compliance, or

- they do have one, but he or she is busy with other priorities and they need someone to manage the day to day issues

What we offer

- Plug short term gaps with experienced staff at short notice. Our staff can be hired as secondees on a temporary basis to plug gaps in the compliance work

- We could do the in-house housekeeping for you; completing VAT returns, European sales lists and Intrastat reporting

- Either on a part-time basis, for a few days a week, full-time for a certain period (e.g. six months) or permanently

A senior team with additional experience and talent

Business challenges

There could be various reasons why more senior level support is needed:- The company faces strategic, operational or IT challenges and needs to adapt fast

- The business has as key objective to get through the acquisition in one piece, to get all of its tax filings done correctly on time and then to build a new supply chain and IT system to support the new operating model and at this stage does not have a full-time indirect tax function

- The indirect tax function is temporary not available (maternity leave, faces conflicting priorities, etc.)

What we offer

- Bring in our senior VAT/IT team:

- Proven industry and consultancy leaders

- Strong technical tax and IT expertise

- Proven project and change management (soft) skills

- To run a project

- To run an effective tax team with the practical knowledge and fresh perspective to help quickly plan and then implement a comprehensive and sustainable plan

- To support in recruiting our replacements (global head of indirect tax, VAT manager) to realize that a client builds up its own department

- We then gradually will leave our roles and support the new tax function in the transition to become successful

Monday, November 30, 2015

SAP VAT Course

Introduction

The SAP VAT determination logic was developed during the 1980’s and, except for the “plants abroad” logic, SAP’s VAT determination logic has changed little. This is in stark contrast with the significant changes made to VAT rules and business models over the same period. With the aim of creating new sales markets and achieving cost savings, business activities are spread all over the world.

Cross-border chain transactions with third parties or within a company (intercompany transactions) have become the rule rather than the exception. The above means that often practical solutions have to be found within the set-up of SAP regarding indirect tax.

Phenix Consulting possesses practical experience and understands SAP's possibilities, but also its limitations and thus the capability to free up resources, reduce manual activities and manage risks.

Program

- Developments in the technology market - this section will elaborate on developments and trends in the technology market that have an impact on the indirect tax function of organizations. Examples include changing business models, but also developments in the approach and processes followed by tax authorities.

- Indirect tax functionality in SAP - learn about the opportunities that standard SAP offers to support the Indirect Tax process, but also addresses the limitations of standard SAP.

- Practical work-arounds - discussing best practice work-arounds, but also risks and opportunities of these work-arounds on quality of the indirect tax process.

- Tax software - overview of software solutions (tax engines) available in the market including their advantages and disadvantages.

The training is interactive. Sufficient time is allocated for answering specific questions and issues that you encounter in your organization.

Our offering

We offer the following models:

- SAP VAT basic training - 4 hours - the following key VAT concepts and functionalities of SAP and VAT will be discussed:

- Standard SAP design

- Standard VAT drivers

- VAT on Sale

- VAT on Purchases

- VAT on FI-Only

- In-depth session - in addition after interviewing and understanding your own operating business models and the design and implementation of SAP your current issues will be discussed and recommendations provided how to come to improvements

- Workshop - the workshop will be completely focused on your 'As Is' and how to get to the 'To Be'. We will provide insight in normative controls, practical workarounds and VAT tools available in the market (e.g. Vertex, OneSource, Meridian and Taxmarc by PwC).

Audience

This training focuses on the tax function, (SAP) IT staff, finance staff, sales staff and Internal Audit.

See for further detailed information

- 'SAP review'

- SAP implementation,

- ERP systems and tax engines

- When is standard SAP (in)sufficient?

- SAP and triangulation

- Indicate import and export during chain transactions

- SAP and 'plants abroad

- SAP checklist for VAT rate change

- Everything you always wanted to know about VAT in SAP * but were not aware to ask

- Tax engines questions to ask before you commit

- Reporting functionality for VAT, EC sales lists and Intrastat and SAP

- Intrastat and SAP

Sunday, November 22, 2015

OECD VAT/GST Guidelines 2015

In the Statement of Outcomes of this meeting, they urged the OECD to finalise the work on the remaining elements of the Guidelines and to present the completed Guidelines for endorsement at the next meeting of the Global Forum.

This work has been carried out since April 2014 and the resulting new elements of the Guidelines have been merged with those that were endorsed at the 2014 Global Forum to form a fully consolidated draft.

This consolidated draft was approved by the OECD’s Committee on Fiscal Affairs (CFA) on 7 July 2015 with OECD and G20 countries working together on an equal footing, and is now presented for discussion at the third meeting of the OECD Global Forum on VAT.

These new elements of the Guidelines notably include a recommended solution for the effective collection of VAT/GST on the remote business-to-consumer sales of digital products by foreign suppliers (B2C Guidelines).

These B2C Guidelines were developed in the context of the OECD/G20 Project on Base and Erosion and Profit Shifting (the BEPS Project).

They were included in the 2015 Final Report on BEPS Action 1 “Addressing the Tax Challenges of the Digital Economy” that was endorsed by G20 Finance Ministers at their meeting on 8 October 2015 in Lima, Peru, as part of the final BEPS Package. OECD VAT/GST Guidelines 2015

Thursday, November 19, 2015

How to make that change

In order to get buy-in from senior management it is often about setting the right priorities, understanding the root cause of underperforming and select a method for measurement that best fits. The deck explains what a tax function could do to get indirect tax higher on the priority list of senior management.

Is it all less challenging when change is initiated and sponsored by senior management itself? For example when the overall business framework is changed (e.g. COSO ERM) or non routine transactions are considered.

The video is 2 minutes slides-only and silent – you may want to use the pause button.

Is it all less challenging when change is initiated and sponsored by senior management itself? For example when the overall business framework is changed (e.g. COSO ERM) or non routine transactions are considered.

The video is 2 minutes slides-only and silent – you may want to use the pause button.

More detail: Where you are and where you want to go

Friday, November 13, 2015

FTI Consulting - Global Indirect Tax Compliance

VAT and other indirect tax compliance is becoming increasingly burdensome. Many businesses now seek to outsource some or all of this burden in order to reduce cost, manage risk and free up time for the in-house finance team.

VAT compliance is an issue that affects businesses from all sectors and in particular, businesses which have numerous trading entities and branches or businesses which trade in multiple locations – in short, anyone with a large or growing number of VAT registrations.

FTI Global VAT Compliance

At FTI Global VAT Compliance we provide everything you need to successfully manage indirect tax compliance and provide a cost effective solution for:

- VAT/GST registration

- Indirect tax reporting - completion and submission of VAT/GST returns and supporting declarations such as Intrastat and EC Sales Lists

- Fiscal representation

What makes us different?

EXPERIENCED TEAM

- Our team is highly experienced, having held senior indirect tax posts within the Big Four and industry.

- We have substantial experience of on-boarding new engagements, working across the EU member states and globally.

- We provide our services to major global businesses and are a recommended service provider for Amazon sales partners.

INDEPENDENCE AND DEPTH

- We are free from audit and assurance relationships. As a result, our clients can always be certain that we will be in a position to represent and advise them whenever required.

- Our European Tax Advisory team is the largest tax team of its type and in addition to VAT compliance provides a full range of tax advisory services to some of the world’s largest businesses.

- We are part of the WTS global tax network, the world’s largest independent tax network, with offices in over 100 countries.

ROBUST CONSISTENT PROCESS

- Your compliance needs will be handled according to one global process using high quality, experienced staff and leading edge tax technology. This delivers complete visibility of the compliance process and enhanced management information.

- From one central point of contact we will register you for VAT wherever necessary, put in place the process for preparing and submitting returns, and where needed, organise the transfer of funds.

PERSONAL SERVICE

- Each client relationship is managed personally through one Global VAT Compliance partner who will provide a single point of contact and will organise the team to deliver the service you need.

- Through our VAT management portal you will always have full visibility of the return status and will have access to archived returns and supporting documentation whenever you need them.

Senior Managing Director

Wednesday, November 11, 2015

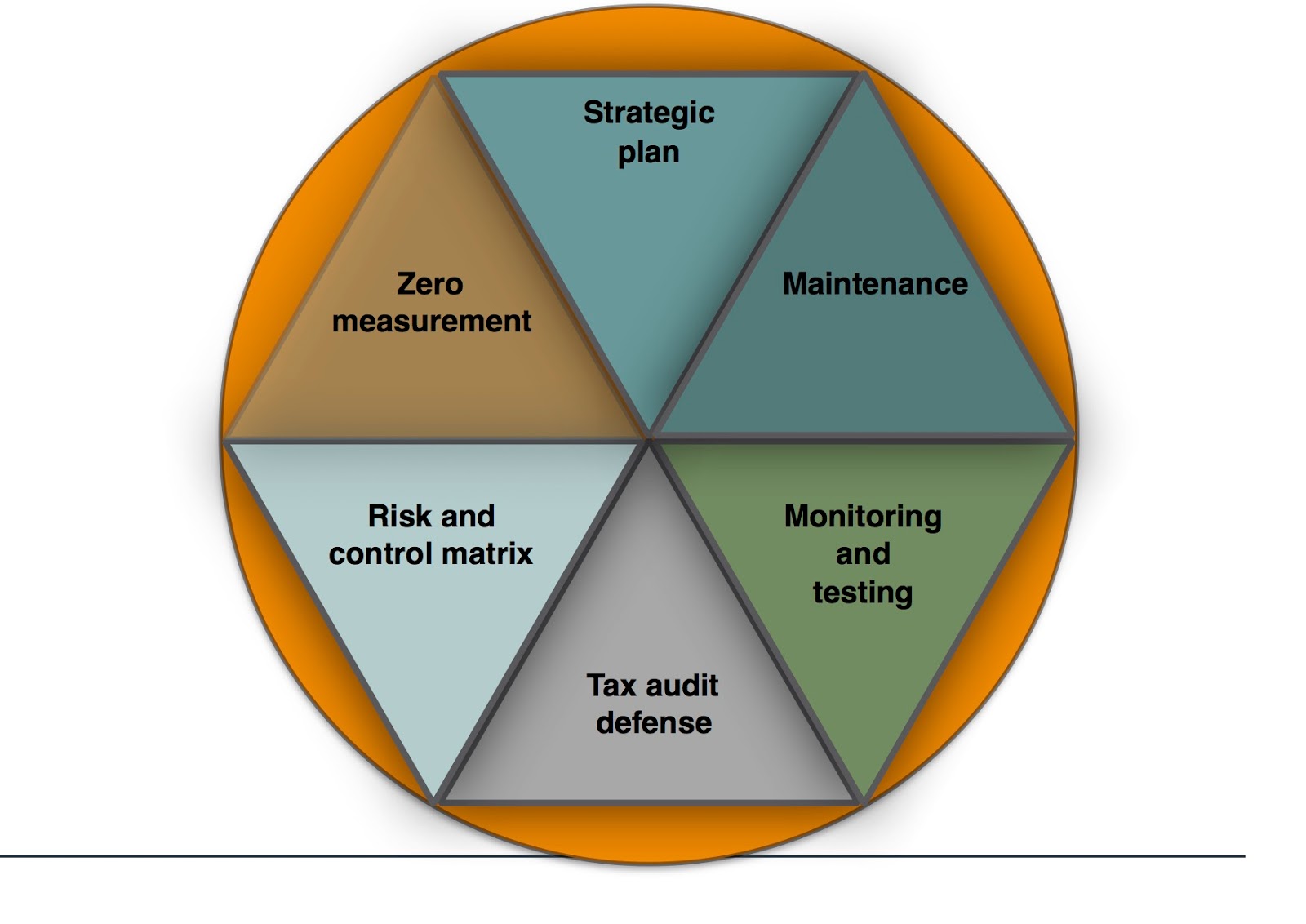

Building blocks of an indirect tax strategic plan

Benchmark information, templates, modules and approaches are shared to support VAT process improvements and meet business objectives

{kind=link}

'Why', 'What', and 'How' of Managing an Effective Indirect Tax function

- Indirect tax strategic plan

- Company's 'governance', 'operation' and 'infrastructure'

- Templates for VAT strategy plan

- Setting the objectives of the tax function

- Structure the tax function

- Audit defense strategy

Wednesday, November 4, 2015

Planning of non-routine transactions

From a Tax Control Framework perspective, for setting up risk based controls, the more unusual the transactions, the greater the tax risks. Examples of non-routine significant business transactions:

Wednesday, October 28, 2015

Where you are and where you want to go

Benchmark information, templates, modules and approaches are shared to support VAT process improvements and meet business objectives

We share our views and best practices.The global tax environment is changing rapidly. How do you anticipate, prepare for and manage these changes? The thought leadership publications on the GITM website could support but also challenge you. You will get access to new views, templates and methods to translate your indirect tax knowledge into workable business processes. In addition, senior management has often competing priorities and indirect tax not always rank high on their priority list. How do you achieve a turnaround and realize their buy-in?

'Why', 'What', and 'How' of Managing an Effective Indirect Tax function:

- A roadmap to indirect tax function effectiveness:

- Where you are and where you want to go

- Planning of non-routine transactions

- Indirect tax strategic plan

- Tax control framework

- Risk management

- Data and technology including VAT and SAP

- Reporting

- Fraud

- Training

- EU developments

Saturday, October 24, 2015

Press Release - Starbucks decision has negative impact on dutch investment climate | AmCham

"This decision is a staggering," says Arjan van der Linde, Chairman of AmCham’s Tax Committee and fiscal spokesman for The American Chamber of Commerce in the Netherlands (AmCham).

"By disregarding OECD rules, the European Commission is creating considerable uncertainty about the tax implications for foreign investment in the Netherlands. This has a direct effect on new investments and future employment. Uncertainty about such a fundamental component of an investment is unacceptable for many companies," predicts Van der Linde.He also highlights the expertise of the Dutch tax authorities,

"The Dutch tax authorities have years of experience with the application of OECD rules and work thorough and carefully in considering transfer pricing requests. A separate APA practice exists. In addition, the Dutch tax authorities are consistent in their approach, with all sorts of coordination groups looking over the shoulder of the inspector. This thorough approach cannot simply be cast aside."AmCham urges the Dutch government to appeal the decision of the European Commission. To prevent interim uncertainty regarding the application of the OECD rules in the Netherlands, AmCham also urges the Dutch government to enter into direct dialogue with the European Commission. Van der Linde:

"The starting point should be that the Commission commits to harmonization of direct taxation within the EU on the basis of an anti-BEPS-directive and not through a disruptive autonomous interpretation of the widely accepted OECD rules."Read further: Press Release - Starbucks Decision Has Negative Impact on Dutch Investment Climate | AmCham

Thursday, October 22, 2015

State aid or not - what about 'reputational tax risks'

Reputational risk is a key element in tax risk management as it is it not only considers individual tax risk but also sees how tax risk may influence the positions in other areas, negatively or positivelyOn June 2014, the European Commission said it had opened three in-depth investigations into tax decisions affecting Apple, Starbucks and Fiat Finance and Trade in Ireland, the Netherlands and Luxembourg respectively.

An U.S. Senate investigation has revealed that Apple, that, "under the agreement Apple has with Ireland", Apple paid a maximum tax rate of 2 percent or less. Apple's annual reports show that over the past three years, Apple paid taxes worth 2 percent of its $74 billion in overseas income.

On his 2008 Presidential campaign trail, Barack Obama made his hostility toward “offshore” jurisdictions very clear:

There’s a building in the Cayman Islands that houses supposedly 12,000 U.S.-based corporations. That’s either the biggest building in the world or the biggest tax scam in the world, and we know which one it is.

European Commission's decision

In the light of the foregoing considerations, the Commission's preliminary view is that the tax ruling of 1990 (effectively agreed in 1991) and of 2007 in favour of the Apple group constitute State aid according to Article 107(1) TFEU [Treaty on the Functioning of the European Union]. The Commission has doubts about the compatibility of such State aid with the internal market. The Commission has therefore decided to initiate the procedure laid down in Article 108(2) TFEU with respect to the measures in question.According to Article 107(1) of the Treaty on the Functioning of the European Union (TFEU), state aid which affects trade between Member States and distorts, or threatens to distort, competition by favoring certain undertakings, is incompatible with the EU Single Market.

The European Commission considers that advance pricing agreements (APAs) should not have the effect of granting taxpayers lower taxation than other taxpayers in a similar legal and factual situation.

Apple says EU probe of Irish tax policy could be 'material' on April 29, 2015 - Apple Inc (AAPL.O) said the European Commission's investigation into Ireland's tax treatment of multinationals could have a "material" impact if it was determined that Dublin's tax policies represented unfair state aid.

Apple has warned investors that it could face “material” financial penalties from the European Commission’s investigation into its tax deals with Ireland — the first time it has disclosed the potential consequences of the probe.

Under US securities rules, a material event is usually defined as 5 per cent of a company’s average pre-tax earnings for the past three years. For Apple, which reported the highest quarterly profit ever for a US company in January, that could exceed $2.5bn, according to FT calculations. [Source: ft.com]

The above, raises the question whether besides evaluating tax risks (level of tolerance) also reputational risks of the company - as part of proper tax risk management - should have been considered when such schemes were setup.

In Apple's defense lots of multinationals have been doing the same and I believed myself that change of the tax system - as those structures are often legally allowed - was the only way to close such gaps.

That changed a bit with the European Commission decision that Luxembourg and the Netherlands have granted selective tax advantages to Fiat Finance and Trade and Starbucks, respectively. These are illegal under EU state aid rules: Fiat and Starbucks ruling.

About change and competencies

Effective tax advice by a tax professional should nowadays not only address the ways of how not paying more tax than necessary and evaluate associated tax risks of implementing such tax planning schemes (rate level of tolerance on a risk scale), but should also take in consideration the impact of such planning on the reputation of the company if it becomes public knowledge.- What is the impact if the tax planning at hand becomes public knowledge?

- What are the consequences if a newspaper or politician picks it up to make statements about lack of 'tax morale' and the company is used as case study?

VAT reputational risks

VAT exposures associated with the wider impact on the company's that arises from a company's actions or errors and have become public knowledge, examples:- Aggressive VAT planning / VAT non compliance becomes public knowledge

- Due to company's VAT failures vendors are not paid in time that might disrupt the business

- Due to company's VAT failures VAT deduction of clients are disputed and assessed by tax authorities

- Failure to drive the optimum relationship with the (indirect) Tax Authorities

Has that - due to the Starbucks and Fiat ruling - now changed and to what extent?

In the indirect tax field, especially value added tax, similar aggressive tax structures were for a long time often approved by (national) case law. That has changed when the European Court of Justice ruled a couple of years ago (ECJ Halifax: February 21, 2006) that the tax advantage had to be revoked or denied.

The indirect tax profession had to change as well and reposition itself to 'manage the numbers of indirect tax' - focus more on risk management - and because of new trends relationships with tax authorities became more important to realize the taxpayer's tax objectives.

Will tax planning become more about ‘being in compliance’ planning?

The new trend is to have an open dialogue between revenue bodies, taxpayers and tax intermediaries. OECD promotes ‘enhanced relationship’ (OECD report: Study into the Role of Tax Intermediaries). Even if the authorities have not embraced such an approach (yet), a proactive mode and using elements of this way of working might not only safe time and money, result in a good relationship but as well mitigate reputational VAT risks.

Further (new) information

- EU Commission State Aid Starbucks Decision – low adjustment is a wash out

- A Mysterious Study in the Code of Conduct Report 1999 and a Rumoured French Connection

- Tax advantages for Fiat and Starbucks are illegal under EU state aid rules

- Starbucks and Fiat Chrysler’s tax avoidance deals to be ruled illegal |The Guardian

- Anticipate, prepare for and lead change

- Tax rulings and other measures similar in nature or effect

- BEPS 2015 Final Reports

- BEPS and Indirect Tax

No VAT on Bitcoin, rules ECJ

Transactions of and for Bitcoin are transactions exempt from VAT, the European Court of Justice (ECJ) has ruled in Case C‑264/14 today.

- Article 2(1)(c) of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax must be interpreted as meaning that transactions such as those at issue in the main proceedings, which consist of the exchange of traditional currency for units of the ‘bitcoin’ virtual currency and vice versa, in return for payment of a sum equal to the difference between, on the one hand, the price paid by the operator to purchase the currency and, on the other hand, the price at which he sells that currency to his clients, constitute the supply of services for consideration within the meaning of that article.

- Article 135(1)(e) of Directive 2006/112 must be interpreted as meaning that the supply of services such as those at issue in the main proceedings, which consist of the exchange of traditional currencies for units of the ‘bitcoin’ virtual currency and vice versa, performed in return for payment of a sum equal to the difference between, on the one hand, the price paid by the operator to purchase the currency and, on the other hand, the price at which he sells that currency to his clients, are transactions exempt from VAT, within the meaning of that provision.

- Article 135(1)(d) and (f) of Directive 2006/112 must be interpreted as meaning that such a supply of services does not fall within the scope of application of those provisions.

Anticipate, prepare for and lead change

Based on the recent UK consultation request it is proposed that large businesses publish their company's tax strategy, the executive signs off of the tax strategy and the business will practice the voluntary code of conduct as discussed earlier in a previous article "Improving large business compliance".The consultation request - when a company's tax strategy is in the end actually published and what currently proposed is in force - should be seen in my view as a 'tax trend beyond UK' also when this is read in combination with other (e.g. OECD) initiatives. Let me explain.

The impact goes beyond the UK when the company's tax strategy is actually published on either the business website or in the annual report. Some quotes from consultation document:

- The strategy should set out the business’s attitude to tax risk, its appetite for tax planning and its approach to its relationship with HMRC.

- It may also cover the governance framework describing the way a business takes decisions on taxation. The research found that “businesses with a greater appetite for risk tend[ed] not to have written (or published) tax strategies, while those with lower risk-appetite tended to have more formalised strategies.

- Businesses will be required to inform HMRC as and when it is published.

- It also shows us that increased scrutiny of tax strategy by a business’s Board actively discourages aggressive tax planning, with businesses stating that tax was now of “particular concern for senior management.

- Building on this, the proposal is to include a requirement to have a named individual at Executive Board level who is responsible for owning and signing off the tax strategy. This will further encourage bringing responsibility for tax into the boardroom and align with the best practice many businesses already exhibit.

- The proposed requirement for Board-level oversight echoes the existing Senior Accounting Officer (SAO) regime, which provides assurance that a business has adequate tax accounting arrangements in place. The SAO regime does not, however, extend to a business’s tax strategy. It is our intention that this proposal is kept apart from the existing SAO regime.

The SAF-T standard, originally created also by the OECD, is intended to give tax authorities easy access to the relevant data in an easily readable format. This leads to much more efficient and effective tax inspections.

Certain countries have already implemented Standard Audit File for Tax Purposes submission. In Europe: Austria, France, Luxembourg and Portugal.

In line with SAF-T obligations, from 1 January 2016 registered businesses in the Czech Republic will be required to file a new VAT return which will have details of each taxable transaction made with other Czech registered business. The Slovak Republic and Hungary have also introduced similar VAT filing requirements in order to prevent VAT fraud.

- Spain’s plans for VAT Immediate Supply of Information (SII)

- New VAT control ledger in Czech Republic

- Mexico: Everything you need to know about electronic accounting records

The Dutch tax authorities announced on May 19, 2015 that 5,000 of its 30,000 employees will lose their current job, while at the same time 1,500 specialized data analysts will be hired as tax returns will be automatically assessed via data analysis. The world - how we know it - is changing fast.

"A pending reorganization at the Dutch tax authority Belastingdienst will likely result in the elimination of 4,000 to 5,000 jobs. The staff cuts are due to improvements to computer systems that reduced the need for many spot checks done by workers, reports broadcaster NOS. Improvements to information technology infrastructure will lead to better data analysis, and thus more accurate tax assessments, sources told NOS. This should not only reduce the amount of tax evasion, but also increase the amount of tax revenue received by anywhere from hundreds of millions to billions of euros every year."

Initiatives and views

- Final Reports BEPS

- State aid or not - what about 'reputational tax risks'

- Tax position exceeds external auditor's materiality

- Examples of public Fiscal Transparency statements

- The Indirect tax impact of BEPS

- Mandatory electronic audit files a worldwide trend

- Tax Compliance Consultation - UK

- UK’s Large Business Compliance Consultation: TEI’s comments

- iBestuur: Belastingdienst zoekt heil in datalaag

Wednesday, October 21, 2015

Tax advantages for Fiat and Starbucks are illegal under EU state aid rules

The European Commission has decided that Luxembourg and the Netherlands have granted selective tax advantages to Fiat Finance and Trade and Starbucks, respectively. These are illegal under EU state aid rules.Commissioner Margrethe Vestager, in charge of competition policy, stated:

"Tax rulings that artificially reduce a company's tax burden are not in line with EU state aid rules. They are illegal. I hope that, with today's decisions, this message will be heard by Member State governments and companies alike. All companies, big or small, multinational or not, should pay their fair share of tax."Following in-depth investigations, which were launched in June 2014, the Commission has concluded that Luxembourg has granted selective tax advantages to Fiat's financing company and the Netherlands to Starbucks' coffee roasting company. In each case, a tax ruling issued by the respective national tax authority artificially lowered the tax paid by the company.

Tax rulings as such are perfectly legal. They are comfort letters issued by tax authorities to give a company clarity on how its corporate tax will be calculated or on the use of special tax provisions. However, the two tax rulings under investigation endorsed artificial and complex methods to establish taxable profits for the companies. They do not reflect economic reality. This is done, in particular, by setting prices for goods and services sold between companies of the Fiat and Starbucks groups (so-called "transfer prices") that do not correspond to market conditions. As a result, most of the profits of Starbucks' coffee roasting company are shifted abroad, where they are also not taxed, and Fiat's financing company only paid taxes on underestimated profits.

This is illegal under EU state aid rules: Tax rulings cannot use methodologies, no matter how complex, to establish transfer prices with no economic justification and which unduly shift profits to reduce the taxes paid by the company. It would give that company an unfair competitive advantage over other companies (typically SMEs) that are taxed on their actual profits because they pay market prices for the goods and services they use.

Therefore, the Commission has ordered Luxembourg and the Netherlands to recover the unpaid tax from Fiat and Starbucks, respectively, in order to remove the unfair competitive advantage they have enjoyed and to restore equal treatment with other companies in similar situations. The amounts to recover are €20 - €30 million for each company. It also means that the companies can no longer continue to benefit from the advantageous tax treatment granted by these tax rulings.

Furthermore, the Commission continues to pursue its inquiry into tax rulings practices in all EU Member States.

It cannot prejudge the opening of additional formal investigations into tax rulings if it has indications that EU state aid rules are not being complied with. Its existing formal investigations into tax rulings in Belgium, Ireland and Luxembourg are ongoing. Each of the cases is assessed on its merits and today's decisions do not prejudge the outcome of the Commission's ongoing probes.

Fiat

The Commission's investigation showed that a tax ruling issued by the Luxembourg authorities in 2012 gave a selective advantage to Fiat Finance and Trade, which has unduly reduced its tax burden since 2012 by €20 - €30 million.

Given that Fiat Finance and Trade's activities are comparable to those of a bank, the taxable profits for Fiat Finance and Trade can be determined in a similar way as for a bank, as a calculation of return on capital deployed by the company for its financing activities. However, the tax ruling endorses an artificial and extremely complex methodology that is not appropriate for the calculation of taxable profits reflecting market conditions. In particular, it artificially lowers taxes paid by Fiat Finance and Trade in two ways:

- Due to a number of economically unjustifiable assumptions and down-ward adjustments, the capital base approximated by the tax ruling is much lower than the company's actual capital.

- The estimated remuneration applied to this already much lower capital for tax purposes is also much lower compared to market rates.

Starbucks

The Commission's investigation showed that a tax ruling issued by the Dutch authorities in 2008 gave a selective advantage to Starbucks Manufacturing, which has unduly reduced Starbucks Manufacturing's tax burden since 2008 by €20 - €30 million. In particular, the ruling artificially lowered taxes paid by Starbucks Manufacturing in two ways:

- Starbucks Manufacturing pays a very substantial royalty to Alki (a UK-based company in the Starbucks group) for coffee-roasting know-how.

- It also pays an inflated price for green coffee beans to Switzerland-based Starbucks Coffee Trading SARL.

Furthermore, the investigation revealed that Starbucks Manufacturing's tax base is also unduly reduced by the highly inflated price it pays for green coffee beans to a Swiss company, Starbucks Coffee Trading SARL. In fact, the margin on the beans has more than tripled since 2011. Due to this high key cost factor in coffee roasting,

Starbucks Manufacturing's coffee roasting activities alone would not actually generate sufficient profits to pay the royalty for coffee-roasting know-how to Alki. The royalty therefore mainly shifts to Alki profits generated from sales of other products sold to the Starbucks outlets, such as tea, pastries and cups, which represent most of the turnover of Starbucks Manufacturing. European Commission - Press release - Commission decides selective tax advantages for Fiat in Luxembourg and Starbucks in the Netherlands are illegal under EU state aid rules

Further information

- Could I Please Get a Fiat for the Price of my Frappuccino?

- The changing tax world and taxpayer's impact

- Tax rulings and other measures similar in nature or effect

- Anticiperen op onze 'nieuwe' belastingwereld

- BEPS 2015 Final Reports

- UK - Improving large business compliance

- Developing a common framework for disclosing tax information

- Reputational risks

Tuesday, October 20, 2015

Bloomberg Business: Starbucks, Fiat Decisions Seen in First Wave of EU Tax Cases

Starbucks Corp. and a Fiat Chrysler Automobiles NV unit are set to be first in the firing line as European Union regulators issue a series of rulings over tax breaks for global companies, including Apple Inc.

The EU may issue decisions against Starbucks and Fiat as soon as next week following a two-year probe into how the companies may have gotten unfair tax treatment from Dutch and Luxembourgish authorities, people familiar with the cases said.

Speculation about the probes intensified this week as Margrethe Vestager, the EU’s competition chief, canceled a scheduled visit to China, citing pressing matters relating to her job. Decisions on whether iPhone maker Apple and Amazon.com Inc. got sweetheart tax deals from Ireland and Luxembourg are expected at a later date, said the people who asked not to be identified because the decision isn’t public.

Apple’s tax strategies were thrown in the spotlight in 2013 when U.S. Senate scrutiny showed that a unit incorporated in Ireland and controlled by a board in California didn’t pay taxes in either location despite having recorded $30 billion in profit since 2009.

The revelations set in motion the EU competition regulator, which opened probes into the iPhone maker, Starbucks’ relationship with the Netherlands, and Amazon.com Inc. and Fiat deals in Luxembourg within months.

Luxleaks

While the EU focused on those four companies, the widespread nature of corporate tax avoidance in Luxembourg was highlighted in late 2014 when thousands of pages of secret fiscal deals the tiny nation struck with companies from around the world, including PepsiCo Inc. and Walt Disney Co., were leaked by an international consortium of journalists.

Seattle-based Starbucks said in a statement that it complies with all relevant tax laws around the globe and pays an “effective tax rate of around 33 percent.” The company said it is cooperating with the EU probe.

Officials from Luxembourg, the Netherlands and the EU declined to immediately comment. Fiat declined to comment beyond previous statements.

The Wall Street Journal reported earlier today that the EU would issue rulings saying the tax deals were improper. Apple raised a flag in April about the potential cost if the company is required to pay past taxes to Ireland as part of the European Commission investigation.

While Apple hasn’t been able to estimate the amount, it could be “material,” the Cupertino, California-based technology company said in a filing with the U.S. Securities and Exchange Commission.

Back Taxes

Any ruling from the EU is unlikely to resolve how much money national governments have to claw back from the companies. Commission officials have previously said the initial decisions will merely contain a formula for national officials to calculate how much back taxes are owed.

While Vestager has promised to move quickly to complete the investigations, she has vowed not to sacrifice quality for speed, as the regulator seeks to build legally sound cases that can fend off legal challenges.

Ireland’s Finance Minister Michael Noonan has vowed to go to court to fight any negative ruling in the Apple case. Whatever happens, “we don’t think it will be damaging,”

Noonan told reporters earlier this month. “If it’s adverse, we think it’s based on very thin legal grounds and we’ll have it before the European Court of Justice.”

In the Starbucks case, the commission said last year that a Dutch unit paid millions of euros to a U.K.-based arm of the company that isn’t taxed in Britain in exchange for a technique to roast coffee beans.

Exaggerated tax-deductible royalty payments for this technique may have allowed Starbucks to unfairly lower its Dutch taxes, the commission said.

In the Fiat case, the commission raised doubts over Luxembourg’s arrangement with Fiat Finance & Trade SA. Fiat said last year it didn’t request a ruling to obtain a tax exemption from Luxembourg and was surprised by the probe. Starbucks, Fiat Decisions Seen in First Wave of EU Tax Cases - Bloomberg Business

Further information

The EU may issue decisions against Starbucks and Fiat as soon as next week following a two-year probe into how the companies may have gotten unfair tax treatment from Dutch and Luxembourgish authorities, people familiar with the cases said.

Speculation about the probes intensified this week as Margrethe Vestager, the EU’s competition chief, canceled a scheduled visit to China, citing pressing matters relating to her job. Decisions on whether iPhone maker Apple and Amazon.com Inc. got sweetheart tax deals from Ireland and Luxembourg are expected at a later date, said the people who asked not to be identified because the decision isn’t public.

Apple’s tax strategies were thrown in the spotlight in 2013 when U.S. Senate scrutiny showed that a unit incorporated in Ireland and controlled by a board in California didn’t pay taxes in either location despite having recorded $30 billion in profit since 2009.

The revelations set in motion the EU competition regulator, which opened probes into the iPhone maker, Starbucks’ relationship with the Netherlands, and Amazon.com Inc. and Fiat deals in Luxembourg within months.

Luxleaks

While the EU focused on those four companies, the widespread nature of corporate tax avoidance in Luxembourg was highlighted in late 2014 when thousands of pages of secret fiscal deals the tiny nation struck with companies from around the world, including PepsiCo Inc. and Walt Disney Co., were leaked by an international consortium of journalists.

Seattle-based Starbucks said in a statement that it complies with all relevant tax laws around the globe and pays an “effective tax rate of around 33 percent.” The company said it is cooperating with the EU probe.

Officials from Luxembourg, the Netherlands and the EU declined to immediately comment. Fiat declined to comment beyond previous statements.

The Wall Street Journal reported earlier today that the EU would issue rulings saying the tax deals were improper. Apple raised a flag in April about the potential cost if the company is required to pay past taxes to Ireland as part of the European Commission investigation.

While Apple hasn’t been able to estimate the amount, it could be “material,” the Cupertino, California-based technology company said in a filing with the U.S. Securities and Exchange Commission.

Back Taxes

Any ruling from the EU is unlikely to resolve how much money national governments have to claw back from the companies. Commission officials have previously said the initial decisions will merely contain a formula for national officials to calculate how much back taxes are owed.

While Vestager has promised to move quickly to complete the investigations, she has vowed not to sacrifice quality for speed, as the regulator seeks to build legally sound cases that can fend off legal challenges.

Ireland’s Finance Minister Michael Noonan has vowed to go to court to fight any negative ruling in the Apple case. Whatever happens, “we don’t think it will be damaging,”

Noonan told reporters earlier this month. “If it’s adverse, we think it’s based on very thin legal grounds and we’ll have it before the European Court of Justice.”

In the Starbucks case, the commission said last year that a Dutch unit paid millions of euros to a U.K.-based arm of the company that isn’t taxed in Britain in exchange for a technique to roast coffee beans.

Exaggerated tax-deductible royalty payments for this technique may have allowed Starbucks to unfairly lower its Dutch taxes, the commission said.

In the Fiat case, the commission raised doubts over Luxembourg’s arrangement with Fiat Finance & Trade SA. Fiat said last year it didn’t request a ruling to obtain a tax exemption from Luxembourg and was surprised by the probe. Starbucks, Fiat Decisions Seen in First Wave of EU Tax Cases - Bloomberg Business

Further information

Monday, October 19, 2015

Tax rulings and other measures similar in nature or effect

On 16.11.15 TAXE Committee will hold an extraordinary committee meeting with various multinational corporations - who have declined previous invitations - to hear their views on recent developments in the corporate taxation in the EU and beyond.

These include, among others, the OECD proposal on the Base Erosion and Profit Shifting (BEPS) Action Plan to the G20 and the ongoing Commission consultation on Common Consolidated Corporate Tax Base (CCCTB).

The Plenary vote is scheduled at Nov II session.

Committee vote on TAXE report - 26.10.2015

Voting session

The committee vote on TAXE report will take place on 26.10.15 in Strasbourg. 1047 amendments were tabled to the draft TAXE report by co-rapporteurs Ms Ferreira (S&D) and Mr Theurer (ALDE) which cover inter alia recommendations on enhanced cooperation and coordination by Member States on tax issues, including tax rulings, a compulsory CCCTB, state aids rules, transparency, country-by-country reporting, tax advisers, protection of whistle blowers and the third country dimensions.

The next meeting of TAXE committee will take place on Monday, 26 October in Strasbourg, from 19.00 to 22.30 in meeting room Winston Churchill (WIC) 200. The vote on the committee's report is scheduled to take place during this meeting which will be webstreamed.

Sunday, October 18, 2015

Australia reacts to BEPS Action Plans

Australian Initiatives

In line with this directive, the Government of Australia has been working on measures to combat multinational tax avoidance by targeting core tax avoidance issues, whilst endeavouring to ensure that Australia remains an attractive and competitive place to do business.The Australian Government has been very vocal in its intention to be at the forefront of tax integrity and the global fight against tax avoidance both from a local-country and multi-jurisdictional perspective.

Comment

The BEPS Actions will revolutionise international tax and transfer pricing practices. Governments all around the world need to act to protect their share of finite global revenues. Whether those governments can work in a cooperative and mutually beneficial manner remains to be seen.However, Australia is determined to be one of the leaders in this area and to shoring up its share of that tax take is clearly its absolute priority. Read further: Quantera Global | Australia reacts to BEPS Action Plans

Relevant background information

'Nederlandse deal met Starbucks is onwettig'| Telegraaf.nl

De EU gaat waarschijnlijk volgende week woensdag beslissen dat Starbucks en Fiat Chrysler van illegale belastingvoordelen hebben geprofiteerd in Nederland en Luxemburg.

Bij de Commissie houdt iedereen de kaken op elkaar, maar duidelijk is inmiddels dat na een onderzoek van meer dan twee jaar de Europese antikartelautoriteit tot de slotsom is gekomen dat de 'tax rulings' die Starbucks en Fiat Chrysler met de Nederlandse en respectievelijk de Luxemburgse fiscus hebben gesloten, onwettig zijn.

Behalve Fiat en Starbucks heeft de Commissie ook Apple en Amazon op de korrel, die gebruik maken van Ierse belastingvoordelen.

(...)

Het grote verschil tussen wettige 'tax rulings' en onwettige is als een belastingdeal is opgezet louter en alleen om eigenlijk nergens belasting te betalen. In het geval van Starbucks zou een in Nederland gevestigd onderdeel van het wereldwijde concern miljoenen hebben doorgesluisd naar een Britse dochter in ruil voor de rechten op het branden van koffie.

(...)

Als de Commissie volgende week doorzet, waar het wel op lijkt, moeten beide bedrijven zich schrap zetten voor forse naheffingen. (...) Het onderzoek van de Commissie kreeg in 2014 een nieuwe impuls toen duizenden pagina’s met geheime belastingdeals in Luxemburg uitlekten, de zogeheten 'Luxleaks'.

Het onderzoek van de Commissie is mede bedoeld om tot 'jurisprudentie' te komen over het maximale belastingvoordeel dat EU-lidstaten aan een onderneming mogen toekennen. Lees verder: 'Nederlandse deal met Starbucks is onwettig'|Nieuws| Telegraaf.nl

Achtergrond info

Bij de Commissie houdt iedereen de kaken op elkaar, maar duidelijk is inmiddels dat na een onderzoek van meer dan twee jaar de Europese antikartelautoriteit tot de slotsom is gekomen dat de 'tax rulings' die Starbucks en Fiat Chrysler met de Nederlandse en respectievelijk de Luxemburgse fiscus hebben gesloten, onwettig zijn.

Behalve Fiat en Starbucks heeft de Commissie ook Apple en Amazon op de korrel, die gebruik maken van Ierse belastingvoordelen.

(...)

Het grote verschil tussen wettige 'tax rulings' en onwettige is als een belastingdeal is opgezet louter en alleen om eigenlijk nergens belasting te betalen. In het geval van Starbucks zou een in Nederland gevestigd onderdeel van het wereldwijde concern miljoenen hebben doorgesluisd naar een Britse dochter in ruil voor de rechten op het branden van koffie.

(...)

Als de Commissie volgende week doorzet, waar het wel op lijkt, moeten beide bedrijven zich schrap zetten voor forse naheffingen. (...) Het onderzoek van de Commissie kreeg in 2014 een nieuwe impuls toen duizenden pagina’s met geheime belastingdeals in Luxemburg uitlekten, de zogeheten 'Luxleaks'.

Het onderzoek van de Commissie is mede bedoeld om tot 'jurisprudentie' te komen over het maximale belastingvoordeel dat EU-lidstaten aan een onderneming mogen toekennen. Lees verder: 'Nederlandse deal met Starbucks is onwettig'|Nieuws| Telegraaf.nl

Achtergrond info

Saturday, October 17, 2015

UK’s Large Business Compliance Consultation: TEI’s comments

Tax Executives Institute (TEI) has provided practical and insightful comments in response to UK’s Large Business Compliance Consultation by HMRC, which is far-reaching. A link to TEI’s comments is provided for reference.

Keith Brockman's key points:

The UK proposal, and similar initiatives, may indeed erode the trust for which the tax authorities are seeking. It would be a novel concept to include the business community in discussions around these proposals prior to drafting, a welcome initiative that would better represent a win-win opportunity.

Additionally, all audits should begin with a formal understanding of the transfer pricing practices of the MNE in that jurisdiction to focus tax queries accordingly and efficiently. As the UK Diverted Profits Tax model has strayed from the OECD’s intent re: the BEPS Action Items, it has nonetheless been followed by other countries.

This proposal may have a similar result, magnifying the concern of MNE’s and merits a detailed review by all MNE’s irrespective of UK business presence. UK’s Large Business Compliance Consultation: TEI’s comments | Strategizing Multinational Tax Risks

Keith Brockman's key points:

- The Consultation is focused on UK HQ companies, although the proposals also apply to non-UK based multinationals (MNE’s).

- The underlying principle is unclear, especially for non-UK based MNE’s, and should be amended accordingly.

- A separate UK tax strategy is an unrealistic expectation for most MNE’s, and will provide little relevance if enacted.

- A UK Code of Practice is also unrealistic for MNE’s.

- UK taxes, paid or accrued, generally bears little relevance to the global effective tax rate and is not relevant.

- UK’s current tools of general anti-avoidance rules (GAAR), Senior Accounting Officer (SAO) tax framework, newly enacted Diverted Profits Tax, a Customer Relationship Manager (CRM) and other anti-abuse rules are already in place and would seem to remedy HMRC’s concerns.

- Special measures are subjective and not subject to a formal independent panel for review prior to execution.

- Board-level accountability may not be practical, while the SAO framework may accommodate this proposal.

- Signing, or not signing, the Code of Practice should not be a trigger for public disclosure or risk assessment.

- The Code of Practice includes determinations that transactions meet the intent of Parliament, an inherently subjective test that may be applied at will regardless of the law.

The UK proposal, and similar initiatives, may indeed erode the trust for which the tax authorities are seeking. It would be a novel concept to include the business community in discussions around these proposals prior to drafting, a welcome initiative that would better represent a win-win opportunity.

Additionally, all audits should begin with a formal understanding of the transfer pricing practices of the MNE in that jurisdiction to focus tax queries accordingly and efficiently. As the UK Diverted Profits Tax model has strayed from the OECD’s intent re: the BEPS Action Items, it has nonetheless been followed by other countries.

This proposal may have a similar result, magnifying the concern of MNE’s and merits a detailed review by all MNE’s irrespective of UK business presence. UK’s Large Business Compliance Consultation: TEI’s comments | Strategizing Multinational Tax Risks

Background information and views

Subscribe to:

Posts (Atom)